When the world shut down, my business did not burn, but it went silent. I discovered the brutal gap between what I thought my business interruption insurance covered and the stark reality of a pandemic. This is my journey through the fine print and the lessons learned. I remember the peculiar quiet of those first few weeks. The phone stopped ringing. The daily rhythm of the door chime, a sound I had taken for granted as the heartbeat of my small boutique, was replaced by an unnerving silence. My business, a physical space built on foot traffic and personal connection, was still standing. There was no fire, no flood, no physical damage to its bricks and mortar. Yet, it was paralyzed. The income vanished overnight, but the fixed costs, the lease, the utilities, the inventory payments, did not. It was then I turned, with a desperate hope, to my business insurance policy, specifically the business interruption coverage. I believed it was my safety net. What I discovered was that I was trying to catch myself in a fall that the net was never designed to handle. The global pandemic was a phantom limb of a disaster, an invisible force that crippled my operations without leaving a single physical scar.

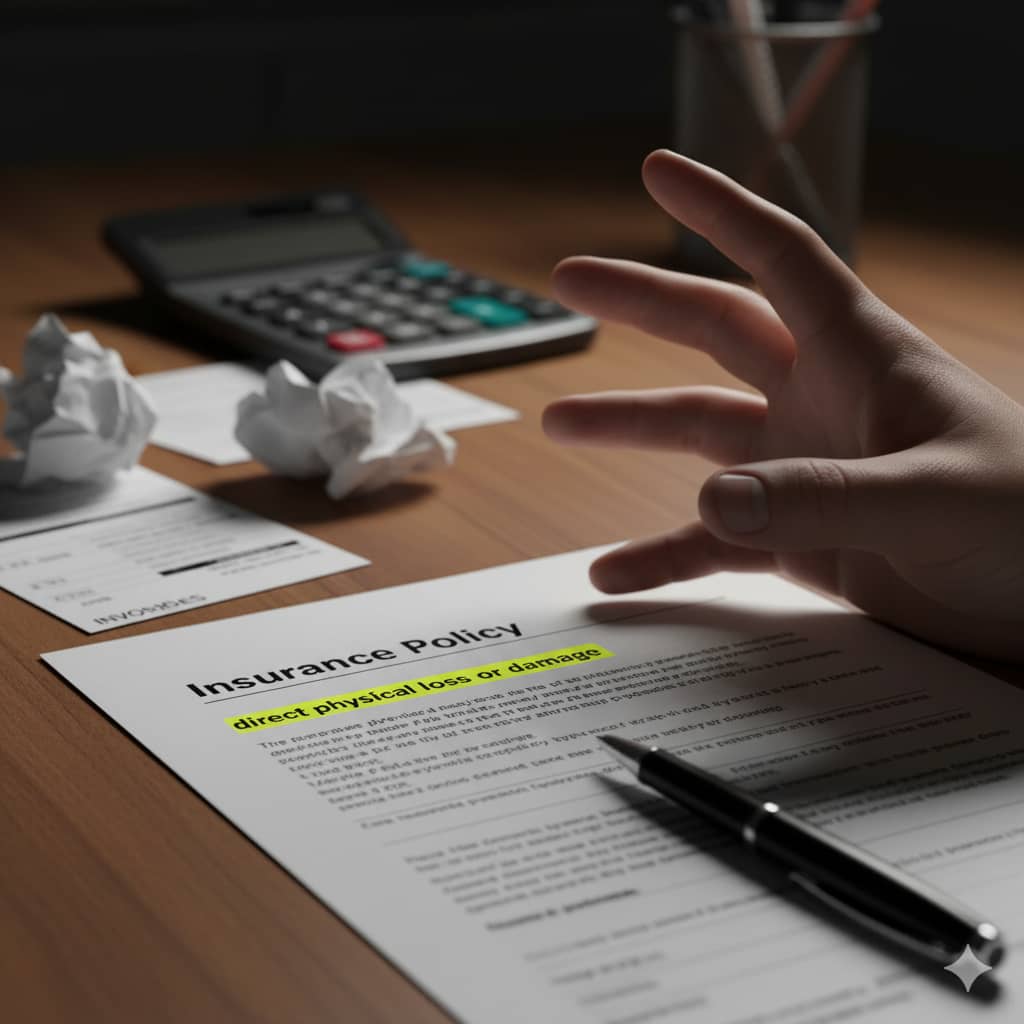

My initial review of the policy was a masterclass in devastating clarity. The language was precise, and it consistently hinged on one critical concept: direct physical loss or damage. This was the trigger, the non-negotiable precondition for a successful business interruption claim. I read the clause over and over, as if the words might morph into something more favorable. A fire damages the roof? Covered. A burst pipe floods the stockroom? Covered. A civil authority shuts down my street because of a gas main explosion next door? Likely covered. But a virus, an airborne pathogen that leaves no visible mark on my property? The insurance company’s position was a resounding no. The virus did not constitute direct physical loss or damage in the way the policy was intended to define it. My premises were still physically intact and could be occupied; they were simply rendered economically unviable by a government-mandated shutdown and a terrified public. I was facing a total loss of function, but in the eyes of the policy, there was no physical alteration to the property itself. This was the chasm between my perception of “interruption” and the legal definition embedded in the contract.

This realization sent me down a rabbit hole of policy addendums and exclusions, where I encountered another critical feature: the virus exclusion. Many commercial property policies, particularly those written in the years following the SARS outbreak, include a specific endorsement that explicitly excludes loss or damage caused by a virus. Seeing that clause in black and white felt like a final, gut-wrenching blow. The insurers had foreseen this exact scenario and had taken deliberate steps to preclude coverage. They had defined the risk, named it, and walled it off. My fight was no longer about interpreting ambiguous language; it was about confronting a deliberate and unambiguous exclusion. The courts would later become flooded with lawsuits from business owners like me, arguing that the government-ordered closures were the direct physical loss, or that the presence of the virus on surfaces did constitute physical damage. The legal battles were, and in some ways still are, complex and divisive. But for me, in that moment, the message from my insurer was clear: this was not a covered peril.

The financial and emotional toll of this coverage gap was profound. It forced me to confront the true nature of risk management. I had insured my business for the disasters I could visualize, the ones that left rubble and water damage. I had failed to insure it against a catastrophe that left everything physically untouched but destroyed the very ecosystem in which it operated. This was a failure of imagination, both mine and, arguably, the entire market’s. In the aftermath, I have become a zealot for a more nuanced understanding of business continuity. I now see business interruption insurance not as a monolithic shield, but as a specialized tool. The experience pushed me to explore alternative and supplementary forms of protection. I have since learned about contingent business interruption insurance, which can cover losses from disruptions to your suppliers or customers. I have investigated parametric insurance, a type of policy that pays out based on the occurrence of a predefined event, like a government-ordered lockdown, rather than proving direct financial loss.

That silent spring was a brutal teacher. It taught me that risk is not just about the integrity of your physical assets, but about the stability of the entire environment in which you operate. My old policy was a map of a world that no longer exists. Today, my relationship with insurance is different. It is a active, questioning partnership. I read the fine print not as a formality, but as a strategic imperative. I ask my broker uncomfortable questions about silent cyber risks, about supply chain fragility, and about non-physical perils. The phantom limb of the pandemic still aches, a reminder that the most dangerous threats are often the ones you cannot see coming, and the ones your standard policy never envisioned. The lesson was expensive, but it was indelible: true resilience lies not in assuming you are covered, but in knowing, with meticulous certainty, exactly where you are not.

References

Tereszkiewicz, P. (2023). Business interruption insurance as a means of spreading pandemic-related losses. *Risk Management, 15*(1), 1-15. https://pmc.ncbi.nlm.nih.gov/articles/PMC10042096/

National Association of Insurance Commissioners. (2023). Pandemic business interruption insurance. https://content.naic.org/sites/default/files/government-affairs-brief-pandemic-bi.pdf

Louaas, A. (2023). A pandemic business interruption insurance. *Journal of Insurance Economics, 8*(2), 117-130. https://pmc.ncbi.nlm.nih.gov/articles/PMC9875781/

Financial Conduct Authority. (2020). Business interruption insurance and the pandemic: UK High Court judgment and implications. https://www.ibanet.org/article/3ad14609-37f4-4487-9eaf-03e9cc669eae

Committee on Capital Markets Regulation. (2021). Pandemic Business Interruption Insurance. U.S. Treasury. https://home.treasury.gov/system/files/311/CCMR-Pandemic-BI-Report-July-2021.pdf