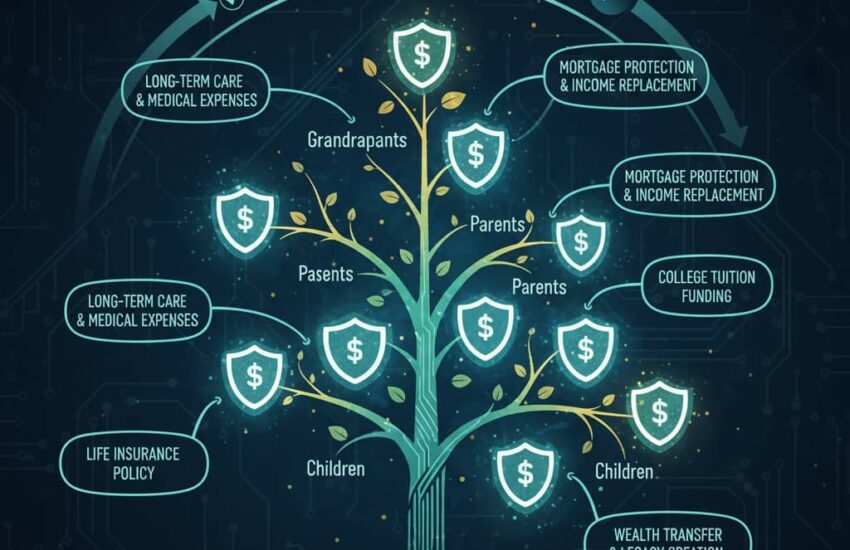

Life insurance can be a powerful tool in estate planning, providing liquidity, protecting heirs, and preserving wealth across generations. Discover strategic approaches to integrate insurance into your legacy plan. I sat with estate planning attorneys as they explained how a family business might need to be sold to pay estate taxes. I witnessed the moment a lifetime of work seemed to hang in the balance. The founders, a couple in their seventies, had built a successful manufacturing company from scratch, but their heirs lacked the liquid assets to cover the substantial tax burden their estate would trigger. That’s when we introduced a strategically designed life insurance policy, not as an afterthought, but as the central solution that would allow the business to pass intact to the next generation. This experience revealed how life insurance, when properly structured, transforms from simple protection into a sophisticated wealth preservation tool.

Life insurance serves as a financial bridge in estate planning, creating immediate liquidity precisely when it’s most needed. Upon your death, policy proceeds provide tax-free funds that can cover estate settlement costs, federal and state estate taxes, and administrative expenses without forcing the liquidation of other assets. I’ve seen families preserve cherished family homes, maintain investment portfolios, and keep businesses operating because life insurance provided the cash that would otherwise need to be raised through fire sales of hard-won assets. This liquidity function becomes particularly crucial for estates heavy with illiquid assets like real estate or privately held business interests.

The strategic placement of policy ownership determines both control and tax consequences. When you own a policy on your own life, the death benefit becomes part of your taxable estate. However, through an irrevocable life insurance trust (ILIT), you can remove the policy from your estate while still providing for your beneficiaries. I worked with a family who established an ILIT that purchased a policy on the patriarch’s life. At his passing, the trust received the proceeds outside of his estate, providing the funds needed to pay estate taxes without increasing the tax burden itself, a sophisticated strategy that preserved millions for his heirs.

For business owners, life insurance addresses multiple estate planning challenges simultaneously. In addition to providing liquidity for estate taxes, it can fund buy-sell agreements, ensuring smooth ownership transitions when a partner dies. I recently helped implement a cross-purchase arrangement where each business partner owned a policy on the others’ lives. When one partner unexpectedly passed away, the surviving partners used the tax-free death benefit to purchase his shares from his estate at a predetermined price, providing his family with fair value while maintaining business continuity.

The selection between term and permanent insurance carries significant estate planning implications. Term insurance works well for temporary needs, such as covering a specific debt or providing protection during the wealth accumulation phase. But for permanent estate planning needs, like paying estate taxes that will exist regardless of when you die, permanent insurance (whole life or universal life) provides the guaranteed protection that won’t expire just when your heirs need it most. I’ve advised clients in their forties to purchase permanent policies specifically for estate planning purposes, locking in insurability and lower premiums while ensuring coverage will be there decades later when their estates have grown substantially.

Life insurance also creates equalization opportunities in complex inheritance situations. When business assets or real estate represent the bulk of an estate but multiple children have differing interests and capabilities, insurance can provide balance. One family I worked with had a farming operation that one son had worked in for years, while two daughters had pursued other careers. Their estate plan left the farm to the involved son while using life insurance proceeds to provide an equivalent inheritance to the daughters, a solution that felt fair to everyone and prevented the heartbreak of forcing a sale of the family legacy.

For high-net-worth individuals, life insurance can leverage annual gift tax exclusions to transfer significant wealth outside the taxable estate. By making annual gifts to an ILIT that then pays policy premiums, you can effectively remove both the premium amounts and the future death benefit from your estate. I’ve watched families systematically transfer millions in potential wealth to the next generation using this approach, all while staying within IRS gift tax limits and maintaining control over the trust terms.

The coordination between life insurance and other estate planning documents requires careful attention. Your will, trusts, and beneficiary designations must work in harmony to avoid unintended consequences. I once reviewed an estate where outdated beneficiary designations contradicted provisions in a newly created trust, potentially diverting assets from intended recipients. Regular reviews, particularly after major life events, ensure your insurance strategy remains aligned with your overall estate plan.

Special needs planning represents another powerful application of life insurance in estate planning. For families with disabled dependents, a properly structured life insurance policy can fund a special needs trust that provides lifelong support without jeopardizing government benefits. I helped create a plan where second-to-die insurance (which pays upon the death of the second parent) would fund a trust that would care for their disabled daughter throughout her lifetime, giving the parents peace of mind that her needs would be met after they were gone.

The role of life insurance in charitable estate planning often goes overlooked. By naming a charity as the beneficiary of a policy, you can make a significant gift at a fraction of the asset’s ultimate value. Alternatively, donating a paid-up policy to a charity during your lifetime can generate an immediate income tax deduction while removing the asset from your estate. I’ve seen clients use this strategy to fulfill philanthropic goals while optimizing their tax situation.

Perhaps the most valuable aspect of using life insurance in estate planning is the certainty it provides in an uncertain process. While investment values fluctuate and real estate markets cycle, life insurance delivers a predetermined amount exactly when needed. This predictability allows for more confident estate planning, knowing that specific financial obligations will be covered regardless of market conditions or timing.

Implementing a life insurance strategy for estate planning requires coordination between your financial advisor, insurance professional, and estate attorney. The most successful plans emerge when these experts collaborate to ensure every element supports your overall objectives. Regular reviews keep the strategy current as tax laws change, family circumstances evolve, and your wealth grows.

Ultimately, life insurance in estate planning isn’t about the death benefit; it’s about the lives it protects and the legacies it preserves. When properly structured, it becomes the financial foundation that allows your values, your business, and your family’s security to endure for generations.

References

Lauenstein Law. (2025, March 19). Life insurance and estate planning: A powerful partnership. Retrieved from https://www.lauensteinlaw.com/news/2025/03/20/life-insurance-and-estate-planning-a-powerful-partnership/

University of Minnesota Extension. (2024, December 31). Life insurance and estate planning. Retrieved from https://extension.umn.edu/transfer-and-estate-planning/life-insurance-and-estate-planning

Western & Southern Financial Group. (2025, October 7). Life insurance for estate planning: Help secure your future. Retrieved from https://www.westernsouthern.com/life-insurance/life-insurance-for-estate-planning

BMC Estate Planning. (n.d.). What is the role of life insurance in estate planning? Retrieved from https://www.bmcestateplanning.com/blog/life-insurance-in-estate-planning

Pacific Life. (2017, December 31). 5 ways life insurance can help with estate planning. Retrieved from https://www.pacificlife.com/insights-articles/5-ways-life-insurance-can-help-with-estate-planning.html